U.S. home prices reached record highs in recent months as the nation’s housing market continues to grapple with persistently elevated mortgage rates and declining sales activity. The contradictory dynamics—soaring prices alongside weak demand—reflect a fundamental supply-and-demand imbalance that shows no signs of resolving quickly.

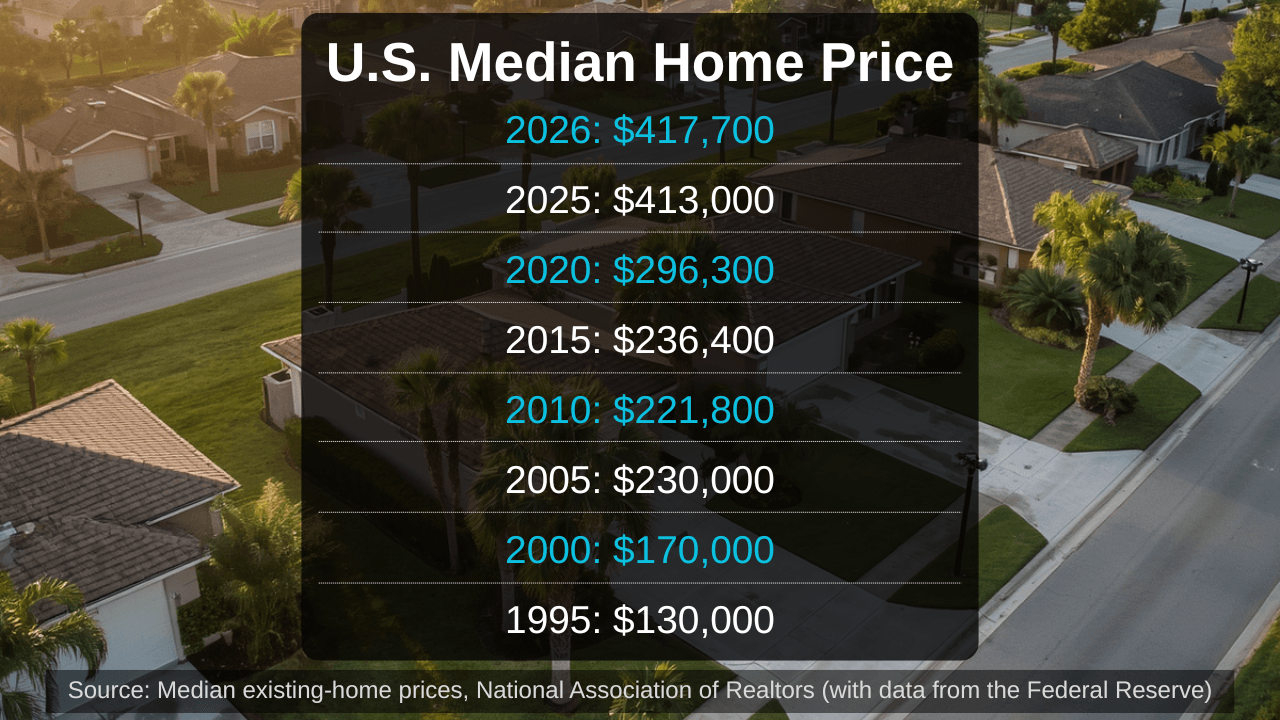

The median price of existing homes sold reached $429,300 in May 2026, marking an all-time high for that month and continuing a remarkable streak of gains. April saw median prices hit $417,700, representing the 34th consecutive month of year-over-year price increases. Even as buying activity has slowed and mortgage rates remain stuck in the mid-6% range, home prices have refused to fall, defying expectations from buyers who have waited years for relief.

The explanation for this seeming paradox lies in the chronically tight housing supply. The shortage of homes for sale has prevented any meaningful price declines despite sharply reduced buyer demand. When homeowners locked in low mortgage rates before 2022, most became reluctant to sell and lose that advantage. This “rate lock-in” effect continues to constrain the supply of available homes, keeping prices elevated even as fewer transactions occur.

In May 2026, existing-home sales reached 4.17 million at a seasonally adjusted annual rate, up 3.2% from April but still well below pre-pandemic norms. Inventory reached 4.5 months of supply in May, up from recent lows but approaching the threshold that would signal a more balanced market. Despite the slight improvement in availability, homes remain scarce relative to historical standards, preventing prices from falling significantly.

Mortgage rates have been the primary headwind. The 30-year fixed-rate mortgage hovered near 6.5% throughout June and early July 2026, up substantially from February’s low of around 5.98%. The escalation stemmed largely from geopolitical tensions and an unexpected spike in inflation driven by Middle East conflicts and rising oil prices. What had been expected to be a year of declining rates instead delivered higher borrowing costs, upending forecasts made just months earlier.

The consequence has been a dramatic pullback in home shopping activity. Existing-home sales in April ticked up only 0.2% from March and remained flat year-over-year, far below the 5 million-plus transactions seen before the pandemic. Consumer confidence deteriorated, with the University of Michigan consumer sentiment index falling to historic lows. Fewer people qualified for mortgages at current rates and prices, narrowing the pool of potential buyers even as home prices climbed.

Yet the market has shown mixed signals recently. June data from Realtor.com indicated asking prices fell 2.5% year-over-year, the steepest annual decline in more than a decade, even as the National Association of Realtors reported the May median price hit a new high. Pending sales, an indicator of future closings, rose 3.7% year-over-year in June for the seventh consecutive month of growth, suggesting that despite high rates and prices, some buyers continued to move forward with purchases.

The divergence reflects stark regional differences. The Midwest and Northeast have maintained relatively tight inventory and strong demand, allowing prices to climb in those regions even through the rate shock. Meanwhile, Western and Southern markets experienced price corrections as affordability limits were tested and builders cleared pandemic-era supply overhangs. Markets like Austin, Texas saw asking prices fall sharply, while Northeastern cities like Providence, Rhode Island posted significant gains.

For first-time homebuyers, the environment has grown particularly challenging. At April’s median price of $417,700, a full-time worker earning the average hourly wage would need the home to cost roughly 5.4 times their annual gross income, far above the historical benchmark of three times income. Even small gains in hourly wages have been offset by rising home values and elevated mortgage rates, leaving the affordability crisis as severe as ever for those trying to enter the market.

Experts remain divided on the path forward. Some forecast that home prices will eventually stabilize or see modest gains of 1-4% in 2026 depending on the forecast source. Others predict stagnation as elevated rates persist and inventory gradually improves. The National Association of Realtors projected only 4% growth in home sales for 2026, a sharp downward revision from an earlier forecast of 14% as mortgage rates failed to decline as anticipated.

The fundamental tension driving the market remains unchanged. Mortgage rates that are historically elevated for the modern era—hovering near 6.5%—suppress buyer demand but also keep sellers on the sidelines, unwilling to give up low rates locked in years ago. This creates a shortage that keeps prices high. New home construction has picked up slightly but not enough to meaningfully relieve supply constraints, particularly in supply-short markets like the Northeast and Midwest.

Without a substantial drop in mortgage rates or a surge in housing construction, the pattern is likely to persist: record-high prices paired with weak sales activity, creating a market where the pain is widespread but distributed unevenly across regions, price points, and buyer demographics.