Tesla reported more than 480,000 vehicle deliveries in the second quarter of 2026, surpassing analyst expectations and suggesting that the company may be turning a corner after nearly two years of declining sales and consumer backlash tied to CEO Elon Musk’s controversial political activities.

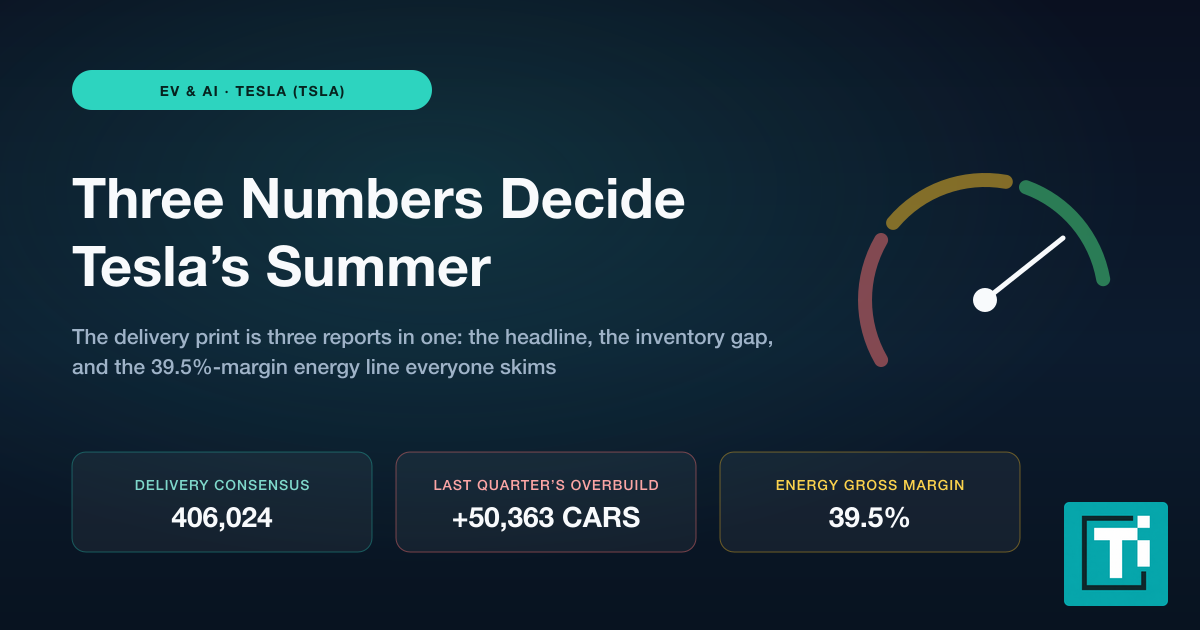

The company delivered 480,126 vehicles globally in the April-to-June period, representing roughly 5.7% year-over-year growth from the same quarter in 2025, when the automaker faced a steep downturn. The figure exceeded the consensus estimate of 406,024 vehicles that analysts had compiled, marking a substantial recovery from the weak first quarter when Tesla managed only 358,023 deliveries.

The improvement appeared to be driven primarily by a rebound in international markets, particularly Europe. After months of steep declines that coincided with Musk’s escalating political involvement and controversial endorsements, European sales showed signs of stabilizing. Higher fuel prices in Europe pushed consumers toward electric vehicles, offsetting some of the damage from the boycott movements and negative sentiment that had plagued Tesla’s image on the continent.

The recovery also reflected modest stabilization in China, where Tesla’s Shanghai factory reported growing shipments after months of weakness. However, the U.S. market continued to face significant headwinds, with demand estimated to be down roughly 20% due to the expiration of the $7,500 federal EV tax credit in September 2025. The loss of this incentive had been one of the biggest obstacles Tesla faced in its home market heading into the second quarter.

Musk’s political activities became a major drag on Tesla’s business beginning in early 2025. The billionaire took on a leadership role in the Trump administration’s Department of Government Efficiency, or DOGE, working to slash federal spending and reduce the size of government. His involvement, combined with his endorsement of far-right political parties in Europe and controversial gestures at Trump’s inauguration, sparked widespread consumer backlash. A grassroots movement called Tesla Takedown organized protests at dealerships globally and encouraged people to sell their vehicles and dump Tesla stock.

Research from Yale University estimated that the controversy surrounding Musk’s political activities could have cost Tesla up to 1.2 million vehicles in sales over a three-year period. The backlash appeared to be particularly severe in progressive-leaning markets like California and across Europe, where Tesla had historically enjoyed strong brand loyalty. Tesla’s brand value plummeted by 36 percent in 2025, dropping from $43 billion to $27.6 billion, according to Brand Finance.

Musk acknowledged the political impact on sales. In various statements, he said that his work with the Trump administration had caused “some blowback” and that he had recognized the need to pull back from his government duties to focus on the company. By May 2025, he had officially stepped back from his advisory position in the Trump administration, signaling a shift in priorities.

The second-quarter results offered some indication that the intensity of the political backlash may be easing. While Tesla’s brand reputation continued to show damage compared to historical levels, the stabilization of deliveries—especially the international growth—suggested that factors beyond Musk’s politics were helping to offset some of the negativity. Morgan Stanley raised its delivery forecast to 413,000 units ahead of the report, citing “very strong” recovery in European and Chinese markets.

Some analysts cautioned, however, that a delivery beat driven primarily by international markets rather than a broad-based recovery might offer only temporary relief. The divergence between struggling U.S. sales and stabilizing overseas demand raised questions about whether Tesla’s fundamental business recovery was underway or whether the company was simply benefiting from temporary favorable conditions like rising fuel prices abroad.

The company’s energy business also showed promise. Analysts expected Tesla to deploy about 13.8 gigawatt-hours of energy storage products in the second quarter, up from a weak 8.8 gigawatt-hours in the first quarter. The energy business carried significantly higher profit margins than vehicle sales, offering an alternative revenue stream as the automaker grappled with increased competition from Chinese rivals like BYD, which had surpassed Tesla as the world’s largest EV maker.

Looking ahead, analysts remained divided on whether Tesla could sustain momentum through the rest of 2026. The full-year consensus called for about 1.65 million deliveries, barely above flat growth for the calendar year. Substantial uncertainty surrounded longer-term projections, with analysts disagreeing by nearly a million vehicles on where Tesla would be by 2030.

Tesla faces several near-term challenges. The company discontinued its flagship Model S and Model X vehicles in January 2026 to free up production capacity for next-generation projects, including the Cybercab robotaxi and Optimus humanoid robot. Neither product has reached significant commercial scale. The company’s primary revenue driver remains the Model 3 and Model Y, which together accounted for more than 96 percent of deliveries.

Investors and analysts remained focused on whether the second-quarter recovery represented a genuine inflection point for the company or simply a temporary bounce driven by favorable international conditions and the absence of major negative news cycles. The coming quarters would likely determine whether Tesla could stabilize sales and rebuild brand value after the turbulent period of late 2024 and 2025, when Musk’s political activities dominated headlines and drove away customers, particularly in markets where environmental values and liberal politics had historically aligned with Tesla ownership.