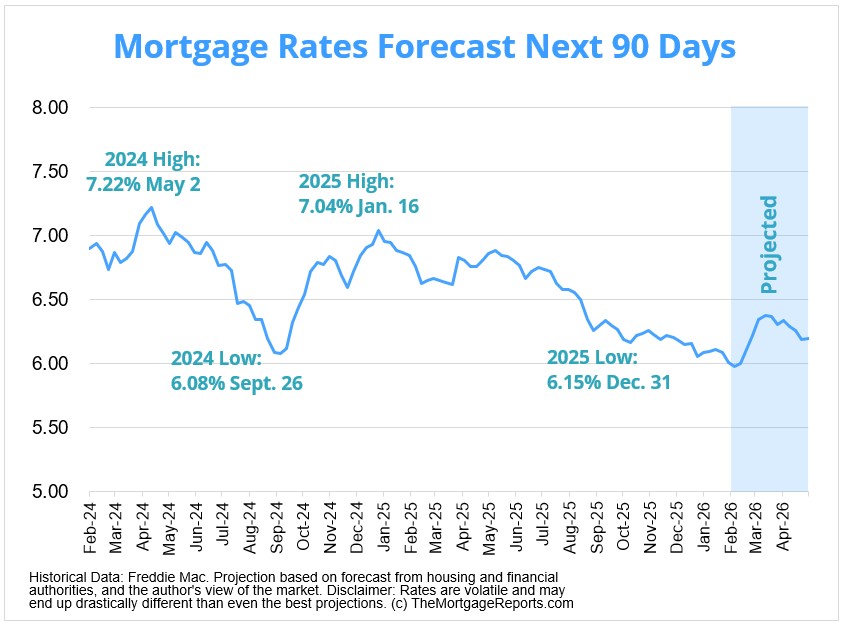

The average 30-year U.S. mortgage rate has risen to 6.49%, marking a significant burden for homebuyers as borrowing costs climb and affordability pressures mount across the nation.

The rate increase reflects broader economic headwinds that have pushed mortgage costs higher throughout the first half of 2026. While recent data shows the 30-year fixed-rate mortgage averaging 6.43% as of early July, the movement to 6.49% underscores the volatility homebuyers have faced in recent weeks. The comparable rate one year ago stood at 6.67%, indicating rates remain elevated despite some improvement year-over-year.

Rising inflation has emerged as the primary culprit behind the climb in mortgage costs. The Consumer Price Index surged to 4.2% in May, the highest level since 2023, well above the Federal Reserve’s 2% target. This spike in inflation has sent bond yields higher, directly pushing up mortgage rates since they track the 10-year Treasury yield closely.

Geopolitical turmoil has amplified inflationary concerns. The conflict between the United States and Iran, which intensified in late February, disrupted global energy markets and sent oil prices soaring. These elevated energy costs rippled through the broader economy, driving up inflation expectations among investors and creating upward pressure on long-term interest rates and mortgage costs.

The Federal Reserve has held its benchmark interest rate steady at 3.50% to 3.75% through multiple meetings in 2026, signaling a pause as policymakers assess inflation’s trajectory. While the Fed does not directly set mortgage rates, its policy decisions influence market expectations and bond yields that drive home loan pricing. Recent economic projections indicate some Fed officials now see the possibility of a rate increase later in 2026 rather than cuts, a reversal from earlier expectations.

The impact of these elevated rates on homebuyers has been pronounced. Monthly mortgage payments have increased substantially compared to earlier in the year, when rates briefly dipped below 6% in late February. For a $450,000 home with a 20% down payment, the difference between a 5.98% rate and the current level translates to roughly $124 more per month in principal and interest payments, adding up to thousands of dollars over the life of a 30-year loan.

Housing affordability has deteriorated significantly. Based on a median family income of $106,800 and a median existing home price of $429,300, monthly mortgage payments at the current rate represent approximately 24% to 25% of typical household income, keeping homeownership out of reach for many potential buyers, particularly first-time buyers struggling with limited entry-level inventory.

Housing market data reflects the strain. Existing home sales have slowed, with applications remaining below year-ago levels in several months. Builder confidence, as measured by the NAHB Housing Market Index, has declined due to affordability pressures. Some homeowners have pulled listings from the market as rising rates and declining affordability cool demand, though inventory has begun slowly improving as pandemic-era locked-in mortgage rates gradually lose their grip on some sellers.

Looking ahead, housing experts and major forecasters generally expect mortgage rates to remain elevated through the remainder of 2026. Fannie Mae projects 30-year fixed rates will average 6.4% for the rest of the year, while the Mortgage Bankers Association forecasts rates at 6.5% for both the third and fourth quarters. Most analysts do not anticipate rates falling meaningfully below 6% in the near term, a significant shift from earlier expectations.

The trajectory of rates will depend heavily on inflation data and any shifts in Fed policy. Additional Consumer Price Index reports scheduled for mid-July and later in the month will provide critical signals about whether inflation is cooling enough to support lower rates. The Federal Reserve’s July 28-29 meeting will offer further insight into policymakers’ thinking, though no immediate rate changes are expected.

Meanwhile, some homebuyers have adapted to the higher-rate environment. Recent data suggests a modest uptick in purchase activity as buyers adjust expectations and recognize that waiting indefinitely for lower rates may no longer be a viable strategy. Some economists note that wage growth expectations and modest home price appreciation forecasts may eventually help improve the affordability picture, though challenges will persist.

For those considering a home purchase or refinance, experts recommend shopping around aggressively among lenders, as rates and fees can vary significantly. Locking in rates when available and avoiding the temptation to wait indefinitely for the perfect rate are strategies financial advisors increasingly encourage, given the uncertainty surrounding future rate movements and the real financial cost of postponing a home purchase.